Research Interests

My research interests are primarily in macroeconomics, monetary economics, and applied time series (macroeconometrics). I am particularly interested in studying the interaction between monetary and fiscal policy, financial markets, and the real economy.

Refereed Publications

Interest Rates, Money, and Fed Monetary Policy in a Markov-Switching Bayesian VAR

[Paper] [Supplement Appendix] [Additional Results Appendix]

The B.E. Journal of Macroeconomics, Volume 23, Issue 2, June 2023, pp. 959-997

Abstract: This paper evaluates the roles of short- and long-term private and government interest rates and inside and outside money in the monetary transmission mechanism. With money and credit markets present, changes in monetary policy set off a chain of relative price and portfolio adjustments affecting output and prices. I study interest rate and money supply rules within this monetary transmission mechanism by estimating several Markov-switching Bayesian vector autoregressions (MS-BVARs) on a quarterly U.S. sample from 1960 to 2018. The best-fit MS-BVAR restricts MS to the impact and lag coefficients of the monetary policy and money demand regressions as well as to the stochastic volatilities (SVs) of the structural shocks. Estimates of this MS-BVAR yield evidence of a SV regime which coincides with NBER-dated recessions. This MS-BVAR also identifies a regime switch in the Fed’s interest rate rule and banks’ demand for outside money around the dot com bust of 2000 and again from the 2007–2009 recession and financial crisis to the end of the sample. Counterfactual simulations show the 2007–2009 recession and financial crisis would have not been as deep and long-lasting if the fed funds rate had been as low as −8 % in 2009 and remained negative from 2010 through 2016.

Working Papers

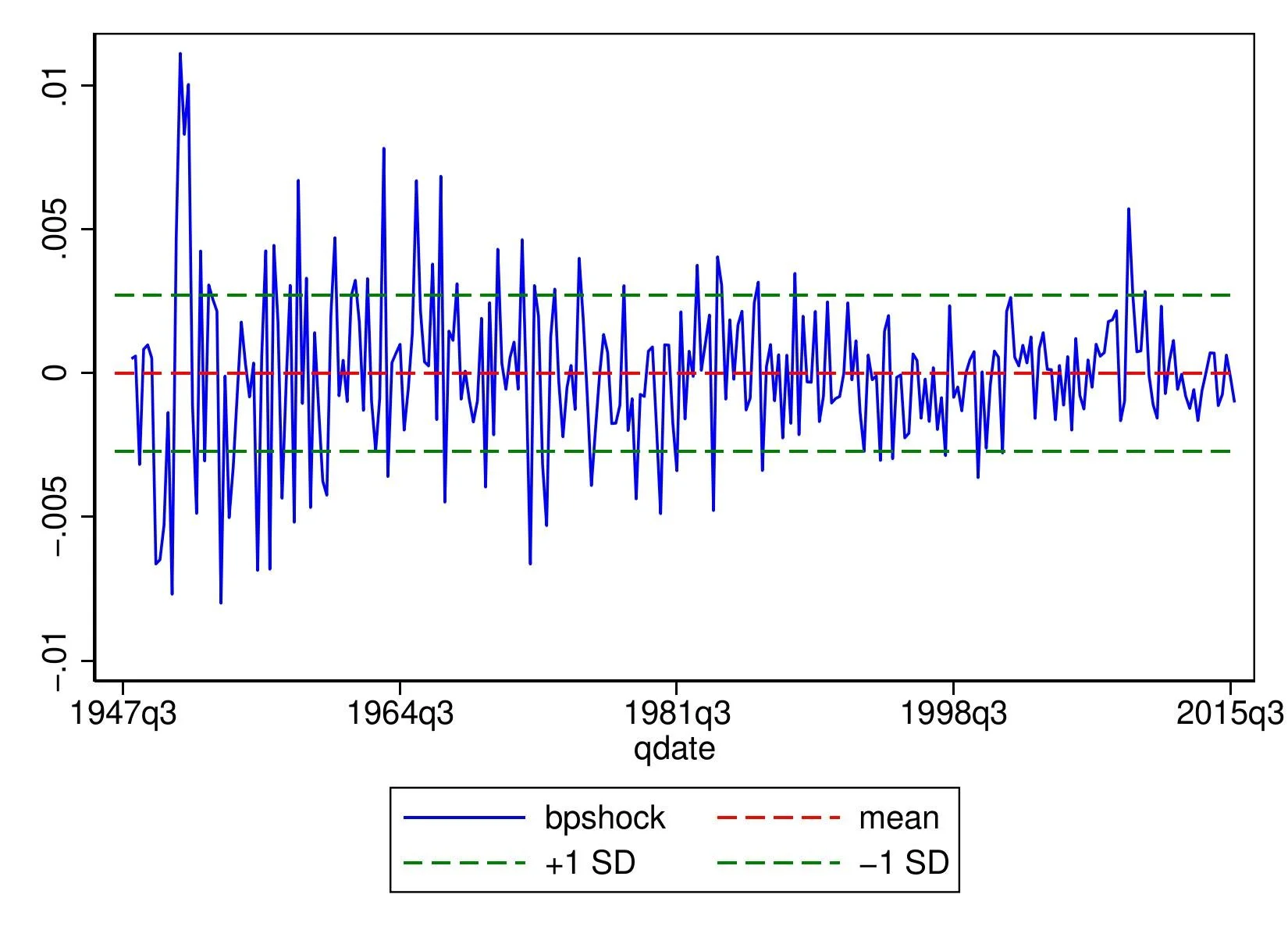

Measuring the Effects of Fiscal Policy Shocks on U.S. Output in a Markov-Switching Bayesian VAR

Latest Draft: 3/18/2026

(Under review)

[Paper] [Supplement Appendix][Conference Slides]

Abstract: This paper estimates Markov-switching Bayesian VARs (MS-BVARs) to measure the effects of fiscal policy shocks on U.S. output from 1960Q1 to 2019Q4. The MS-BVAR addresses fiscal foresight—the tendency of agents to anticipate and react to future policy changes—by endogenously identifying fiscal and macroeconomic regimes whose transition probabilities enter agents’ decision rules. Granger causality tests confirm that regime switching substantially reduces shock predictability, particularly for tax shocks. Government spending multipliers are strongly state-dependent, ranging from 1.4–1.8 during recessions to approximately 1.0 during expansions. Tax multipliers are consistently small and imprecisely estimated across all regimes.

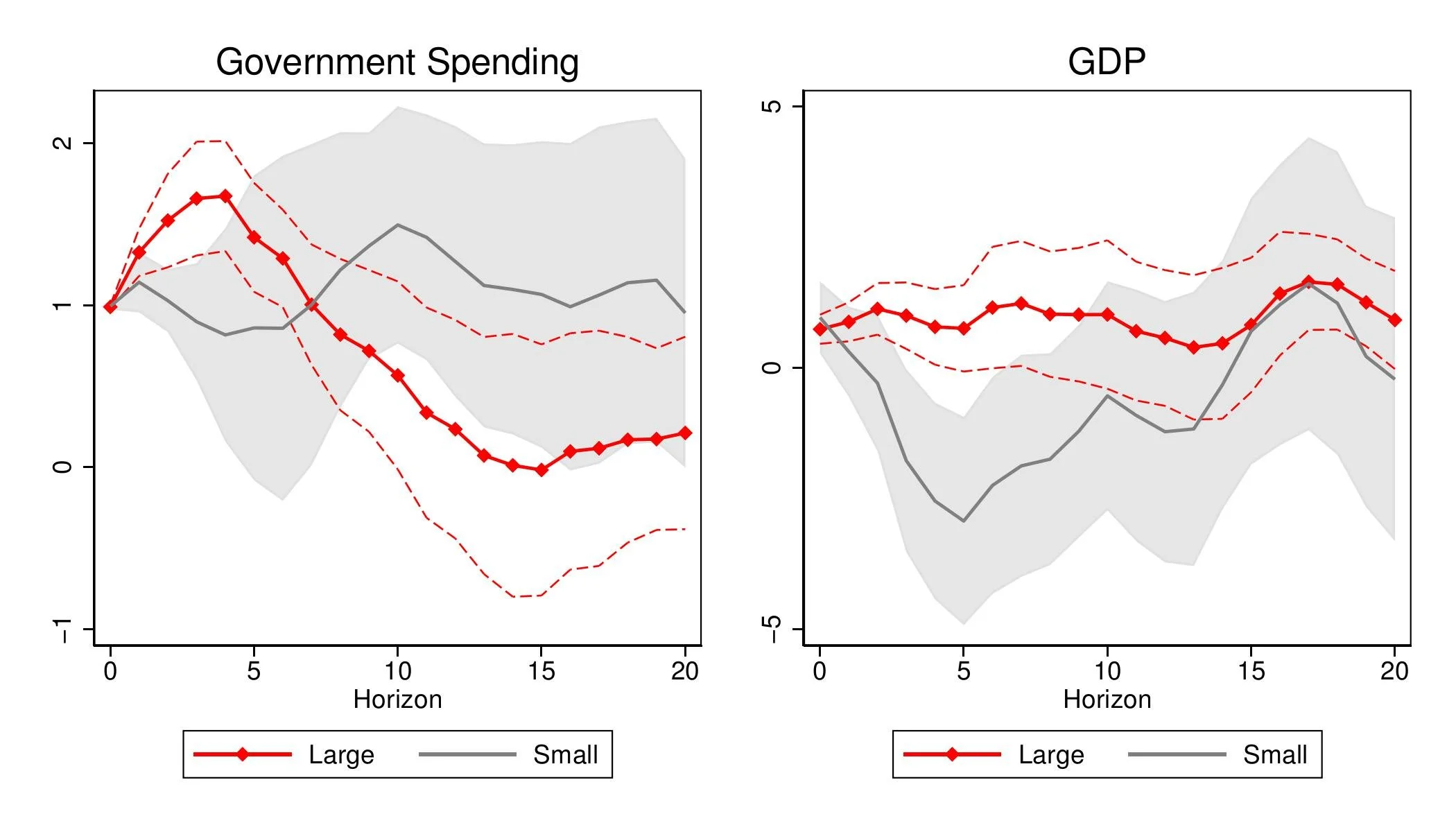

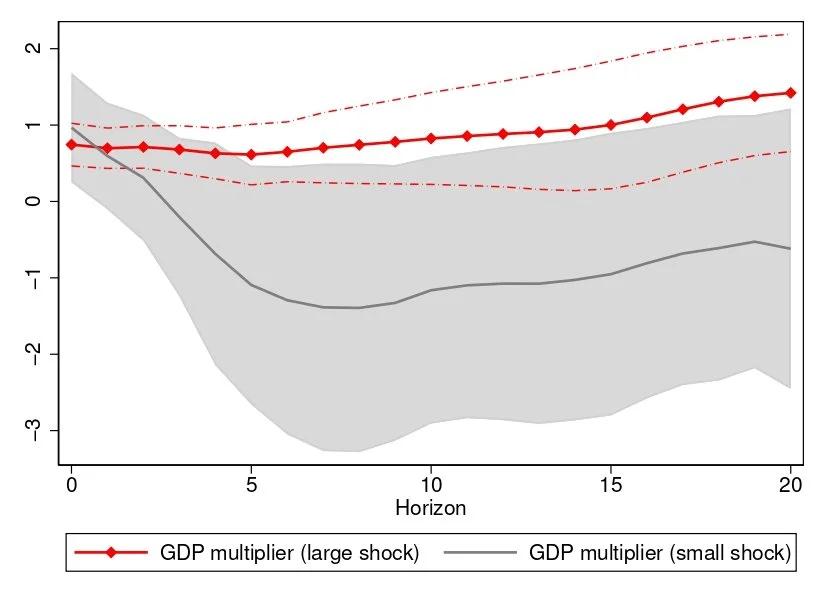

Understanding the Effects of Government Spending Shocks: It’s in the Size as Well

with Xiaoxiao Bai (Mississippi State University) and Sebastian Laumer (University of Richmond)

LATEST DRAFT: 3/20/2026

(under Review)

[Paper][Supplement Appendix][Conference Slides]

Abstract: This paper investigates whether fiscal multipliers depend on the size of the government spending shock. Using U.S. quarterly data from 1947Q1 to 2015Q4, we estimate state-dependent effects of “large” versus “small” spending shocks via local projections. We find strong evidence of size-dependent fiscal multipliers. Large shocks generate a cumulative output multiplier of approximately one, driven by crowding in of private consumption. Small shocks produce a negative, though imprecisely estimated, multiplier consistent with crowding out. These results suggest that the magnitude of a fiscal intervention is a critical determinant of its effectiveness, providing empirical support for a “go big or go home” approach to fiscal stimulus.

Work in Progress

“When Money Matters Differently: Asymmetric Effects of Inside and Outside Money Shocks” (with Joshua Hendrickson)

“Same Policy, Different Stories: The Heterogeneous Impact of Monetary Policy Across U.S. Industries” (with Ryan Rholes)

“Money, Liquidity, and U.S. Monetary-Fiscal Policy Interactions”